You have had your last day of service with the NSW Police Force (NSWPF) and you remain certified as having no capacity for work. So, let’s talk about the different scenarios that might be applicable to you as you transition out of the Force.

The maximum weekly compensation amount is set by the State Insurance Regulatory Authority (SIRA) and indexed twice each year in April and October.

The following information relates to sworn NSW Police Officers only as they are considered exempt workers in the Workers Compensation Act 1987 No 70 – NSW Legislation. If you are an administrative employee of NSWPF, please see the SIRA claims management guide or consult your case manager regarding your benefits.

Find more information about career transition for NSW Police Officers on our website, including managing other aspects of your finances.

Click on each of the below options to learn more about the different scenarios that might be applicable to you.

Up to 26wks no capacity, no income protection

Scenario 1 – up to 26 weeks with no capacity for work and you DON’T have an income protection claim

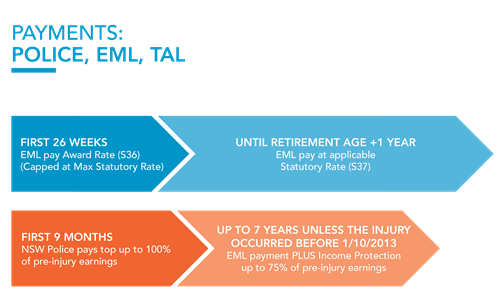

During the first 26 weeks of incapacity, the weekly benefit paid will be:

Current Weekly Wage Rate (CWWR); or

The maximum weekly compensation amount, whichever is the lesser

During the first 26 weeks of incapacity, Police Officers are entitled to weekly benefits equal to 100% of their pre-injury salary (excluding overtime, shift work, payments for special expenses and penalty rates). This is known as the Current Weekly Wage Rate (CWWR).

The first 26 weeks do not need to be consecutive. Any period where you have no capacity for work counts towards the first 26 weeks of incapacity.

For example, a Police Officer had no work capacity for 12 weeks. The Officer then returned to work on a Recover @ Work Plan for 8 weeks before being downgraded to no capacity for work. In this scenario, the Police Officer is still eligible for a further 14 weeks of payments at the CWWR (full pay) before entitlements of the first 26 weeks of incapacity are exhausted.

Up to 26wks no capacity with income protection

Scenario 2 – up to 26 weeks with no capacity for work and you DO have an income protection claim

You will be paid by EML as per Scenario 1 until you either:

Exceed a total of 9 months of total incapacity; or

Change your capacity to work

When either of these circumstances arise, you will only receive an income protection payment if your entitlements under workers compensation are less than 75% of your normal salary (CWWR).

More than 26wks no capacity, no income protection

Scenario 3 – more than 26 weeks with no capacity for work and you DON’T have an income protection claim

After the first 26 weeks of incapacity, the weekly benefit paid will be:

a fixed rate known as the ‘statutory rate’; or

90% Current Weekly Wage Rate (CWWR), whichever is the lesser.

For former NSW Police Officers, this is usually the statutory rate.

More than 26wks no capacity with income protection

Scenario 4 – more than 26 weeks with no capacity for work and you DO have an income protection claim

You will be paid as per Scenario 3 PLUS your income protection entitlement.

In addition to statutory rate payments paid to you by EML, you are entitled to top-up payments based on your current capacity for work and the time elapsed since your date of injury.

Top-up payments are paid to you either by NSWPF or TAL insurance.

The first 9 months following date of injury

Injured NSW Police Officers cannot be medically retired within nine months of injury.

Under the provisions of an income protection claim you are entitled to receive from NSWPF a top-up to 100% of your normal salary for the duration of the income protection waiting period (nine months) from the date of disablement (first time you had no capacity for a consecutive period of 7 days).

As you approach nine months after the date of your injury, you will receive an income protection information package from NSWPF. It is important that you complete the claim forms in the package and send them back to the return address as soon as possible to enable your claim to be assessed quickly.

For assistance completing the income protection forms, please contact the NSWPF Income Protection Unit on 02 8835 8400.

Income protection payments are made monthly in arrears. When you reach the nine-month milestone you will experience four weeks of reduced pay until your first income protection payment is made.

It is important to prepare your finances for an initial period of reduced pay.

More than nine months from date of injury

Under the provisions of an income protection claim, nine months after your date of injury you are entitled to receive approximately 75% of your pre-injury ordinary earnings (CWWR) for a maximum period of seven years, or until you reach 60 years of age.

Income protection payments are managed and paid to you by TAL insurance and are in addition to your statutory rate entitlements.

Income protection payments are made monthly, four weeks in arrears and are typically the difference between the amount paid by EML and your Income Protection Salary Rate.

Your Income Protection Salary Rate is: your salary, less loading and allowances, plus 17%, except for commissioned officers.

For more information, contact your TAL Case Manager or TAL Existing Customer Enquiries on 1300 209 088. You can also visit the TAL website for more information about TAL income protection.

Case study 1 – no capacity since date of injury

Background

Jane sustains an injury at work and her doctor certifies her as having no capacity for work.

Jane receives various forms of treatment and has preliminary discussions about returning to work. However, five months later she is still not fit for work at NSWPF. In consideration of Jane’s long-term health outcomes, her doctor recommends she is medically retired from NSWPF and encourages Jane to consider alternate work options when she is fit for work.

After Jane’s last day of service with NSWPF she continues to have no capacity for work.

What payments are received?

Jane is paid her normal salary by NSWPF for the period she is still employed. Up to a period of 26 weeks NSWPF recoup this at the CWWR from EML.

For the period from week 27 to nine months, Jane continues to be paid her normal salary by NSWPF however they only recoup the statutory rate from EML.

After Jane’s last day of service with NSWPF, having satisfied the requirements for income protection, she receives the applicable statutory rate paid fortnightly from EML, plus a monthly payment (paid in arrears) from TAL topping up Jane’s payments to her Income Protection Salary Rate.

These payments continue until Jane either:

has a change in capacity for work; or

finds new employment; or

reaches the end of her seven-year income protection benefit period.

Case study 2 – attempted return to work

Background

Craig sustains an injury at work and his doctor certifies him as having no capacity for work for four weeks.

Following treatment, he feels much better and is keen to get back to work. Craig’s IMA helps put together a Recover at Work Plan and after four weeks off work, he returns on restricted duties.

After some ups and downs and 12 weeks on restricted duties, Craig consults his doctors and downgrades to having no capacity for work.

Despite further treatment, Craig is unable to return to work and is recommended for medical retirement.

Craig’s last day of service with NSWPF is nine months after initially going off work.

What payments are received?

Craig is paid his normal salary by NSWPF for the period he is still employed. For the first four weeks of incapacity, NSWPF recoup this at the CWWR from EML.

For the period that Craig is on a Recover at Work Plan he continues to be paid his normal salary but NSWPF only recoup the s40 top up value from EML (see capacity scenarios below for more info).

At the time that Craig is certified as having no capacity to work, he still has 22 weeks (26 weeks less the initial four weeks) of normal salary benefits remaining. As such, Craig continues to receive his normal salary from NSWPF who then recoup this from EML.

After Craig’s last day of service with NSWPF, having satisfied the requirements for income protection, he receives the applicable statutory rate paid fortnightly from EML, plus a monthly payment (paid in arrears) from TAL topping up Craig’s payments to his Income Protection Salary Rate.

These payments continue until Craig either:

has a change in capacity for work; or

finds new employment; or

reaches the end of his seven-year income protection benefit period.

> Return to managing finances, NSW Police career transition home.